Overview

Revenue should be recognized when the service or goods are delivered. Deferred revenue tracks payments received before delivery, which is especially important for SaaS companies selling annual subscriptions. This guide explains how to model recognized and deferred revenue in Francis.Basics

Recognized and deferred revenue

According to accounting principles, revenue is recorded when the service or goods are actually delivered. This ensures that income reflects real business activity rather than just invoicing or payment timing. Deferred (unearned) revenue represents amounts invoiced in advance of delivery. It appears as a liability on the balance sheet until the service is performed or the product is delivered. At that point, deferred revenue shifts from the balance sheet to recognized revenue on the income statement. In practice, we consider the following milestones:- Booking: A contract is signed, but no financial entry is recorded.

- Contract start and end dates: These specify the service period and define when revenue should be recognized based on performance obligations.

- Invoice: An invoice is sent. If payment is due later, it creates accounts receivable.

- Recognized: Revenue is recorded on the income statement once the performance obligation is met, typically tied to the contract period or specific delivery milestones.

- Receivables is paid: The customer pays, affecting cash flow but not revenue recognition.

Examples

Annual membership with events

Imagine a running club selling annual memberships that include events in March, May, and August.- Initial Payment (January): The club invoices and receives payment upfront, recording it as deferred revenue.

- Events Throughout the Year: When each event occurs, one-third of the annual fee is recognized as revenue, aligning income with the delivery of services.

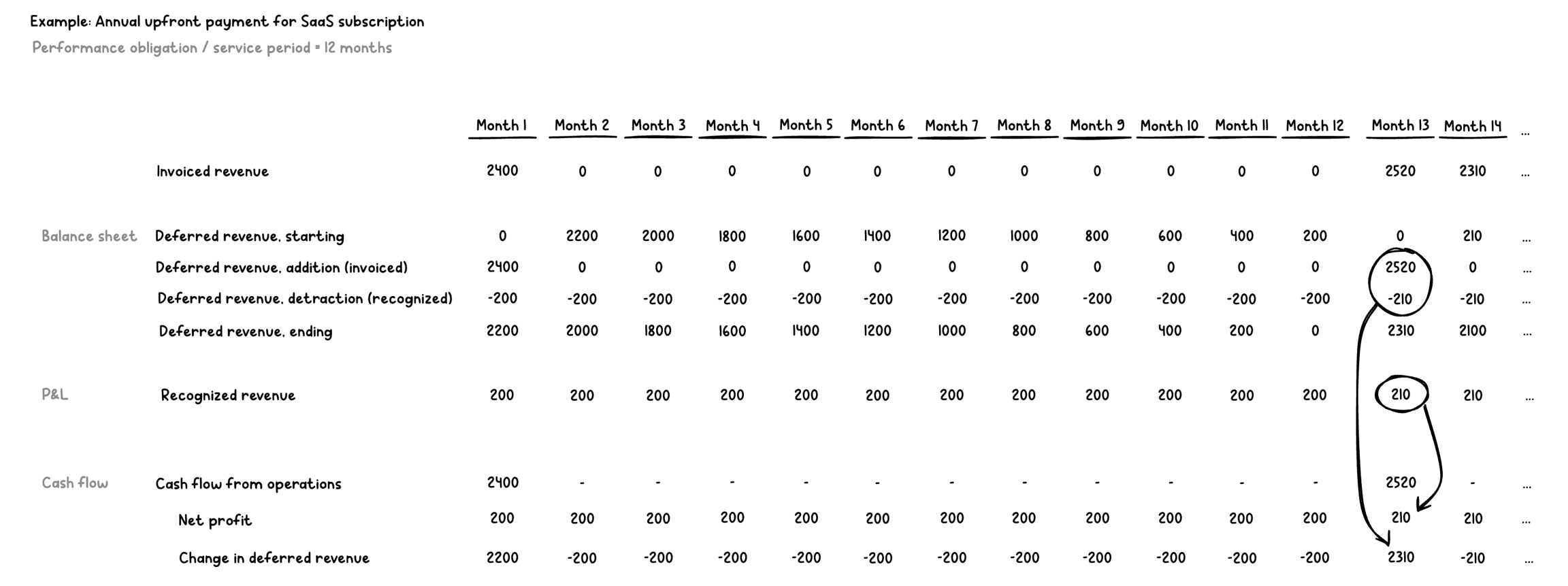

12-month SaaS subscription

Consider a SaaS company selling a 12-month subscription paid upfront.- Initial Payment: The full annual fee is invoiced and recorded as deferred revenue.

- Monthly Recognition: Each month, one-twelfth of the fee moves from deferred revenue to recognized revenue as the service is delivered over time.

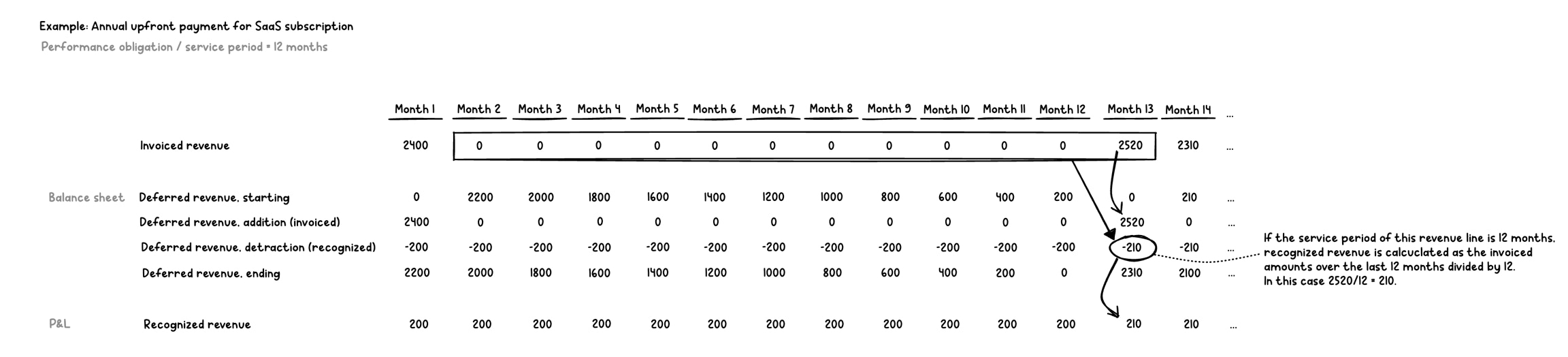

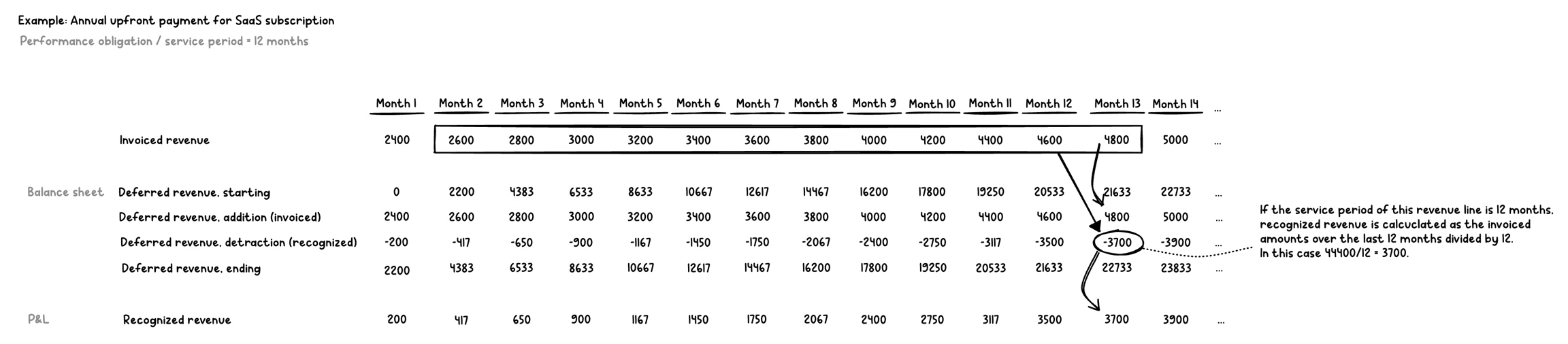

Calculating recognized and deferred revenue

To determine how much revenue to recognize each month, consider the service period (e.g., 12 months) and review the invoiced amounts over that period. By distributing invoiced amounts evenly across the service period, you ensure revenue is recognized in proportion to the delivery of goods or services.

Cash flow effects

Deferred revenue itself doesn’t change how much cash you receive – it only affects the timing of when revenue appears on the income statement. For instance, if a customer pays $2,400 upfront, that cash is received immediately, regardless of how you recognize the revenue over time. On the cash flow statement, recognized revenue contributes to net profit, while changes in deferred revenue appear as a working capital adjustment. If invoices have delayed payment terms, this introduces accounts receivable, which you can model separately.